Like it or not, Artificial Intelligence (AI) is coming to a project near to you. As well as adaptations of the generic tools such as ChatGPT many new tools are being released and established tools upgraded to embed AI in various ways. But care is needed – “Garbage in, Garbage out” can still diminish the value of AI.

Generative AI tool that create content based on their ‘large language model’ need to be trained on quality resources rather than the mass of misinformation floating around the internet. This is not hard to do and can generate impressive results (but be careful of copyright). Most project management tools with embedded AI are built around machine learning (ML) and learn from the data you generate; the more advanced tools then apply AI to create insights.

These enhanced tools bring almost limitless processing capabilities to give meaning to data and help make crucial decisions to achieve project strategies. They can take over various technical tasks allowing project managers to deal with more crucial tasks as well as improving various estimating and risk assessment processes by provide insights from previous projects to enable managers to do a better job. These systems can also assist by keeping track of the project and checking key metrics like budgets, milestones, and other resources.

AI is still improving, and so are AI project management tools. All of this creates numerous benefits for the project management process. However, here are some core benefits you can expect right away.

Better Project Estimations

Improved Scheduling and Planning

More reliable Roadmaps and Budgets

More Predictability

There are a surprisingly large number of tools embedding ML and/or AI, too many to list here! What we have done is augment the Mosaic PM Software and Tools listing to highlight tools with some ML or AI capability – look for the blue – AI – in the categorized listings at: https://mosaicprojects.com.au/PMKI-SCH-030.php

If you know of any additional tools missing from the list (or tools in the list that should be flagged ‘AI’) let me know and I will update the list.

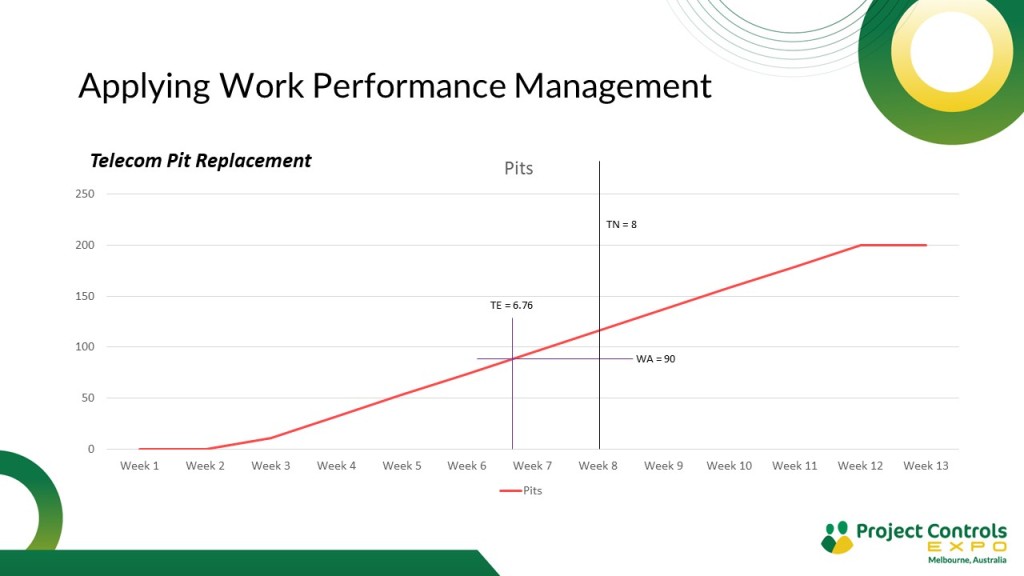

Work Performance Management (WPM) is a methodology developed by Mosaic Project Services Pty Ltd to offer a simple, robust solution to the challenges of providing rigorous project controls information on projects that cannot (or are not) using CPM and/or EVM. It works by setting an expected rate of working using an appropriate metric, then measuring the actual work achieved to date. Based on this data, WPM can assess how far ahead or behind plan the work currently is, and using this information calculate the likely project completion date and VAC.

The basis of the calculations used in WPM are the same as is used in Earned Schedule (ES), however, WPM is much simpler to set up and use. The only two requirements to implement WPM are:

A consistent metric to measure the work planned and accomplished, and

A simple but robust assessment of when the work was planned to be done.

Our latest article, How WPM Works, explains in detail the processes and calculations used in WPM, and the outputs produced.

Understanding the current status and projected completion is invaluable management information for Agile and other projects where CPM schedules are not used, and even where a project has a good CPM schedule in place this additional information is useful. Then by plotting the trends for both the current variance (WV) and VAC management also knows how the project is tracking overall.

Based on the information gathered at PC Expo Melbourne, Mosaic’s comprehensive project management software listing has been groomed and updated. A brief description and links to the developers’ web sites are provided for each entry.

Our mission is to make this listing the definitive categorized listing, so if we’ve missed a tool let us know! We do not try to work out what tool is ‘best’ – this depends on the needs of the project, and no one pays to be included.

Work Performance Management (WPM) is a new project controls tool that is being developed by Mosaic Project Services. WPM is designed to calculate the current status, and predicted completion date for any project in a consistent, repeatable, and defensible way. It is primarily intended for use in projects, applying Agile or Lean Construction management approaches, where traditional CPM scheduling cannot be used effectively, but will add value on most projects. The types of projects where WPM can provide an effective controls tool include:

Relatively small projects requiring a straightforward controls system

Large projects with a single primary deliverable that is easy to measure

Large projects using CPM where there is a need to overcome the CPM optimism bias[1]

All project applying Agile[2] and Lean Construction approaches where the project team determine the sequence of working

Distributed projects[3] where CPM is inappropriate, and management has chosen not to use the ES extension to EVM.

WPM is an easy to use, robust, performance measurement system. The two requirements to implement WPM are:

A consistent metric to measure the work planned and accomplished, and

A simple but robust assessment of when the work was planned to be done

Based on this data, WPM can calculate how far ahead or behind plan the work currently is, and based on this information, the likely project completion date (assuming work will continue at the current rate). Recording the status and expected completion at each update provides reliable trend information. This means there is no longer any excuse for, a project team, senior management, and/or the organization’s governing body, ‘not to know’ how the work of each project is progressing.

Project controls are facing a dilemma, on one hand there is a strong push to make projects agile and adaptive, on the other the need for on time delivery, organisational reporting requirements, and the law of contracts require precision and certainty from project control systems. For a wide range of projects, traditional critical path scheduling (CPM) is no longer fit for purpose, a new controls paradigm is needed.

CPM is based on scientific management concepts. It assumes there is one best way to undertake the work of a project, management know what this is, and their intentions can be modelled in a CPM schedule. While the CPM paradigm remains true for many projects, experience shows there are also many where this assumption is simply not correct including both soft and distributed projects. In this type of project, there is an ongoing level of flexibility in the sequencing of work that can be exploited to the benefit of the project and the client. However, most of the available management tools such as burndown charts, Kanban boards, sprint planning, last planner, etc., are specific to a methodology, focus on optimising work in the short term, and lack a rigorous predictive capability.

This presentation define the characteristics of projects that are not suited to CPM, including agile, adaptive, and distributed projects, and describe an approach for managing this type of project based on agile and lean, while recognising there are likely to be some mandatory sequences that must be followed. WPM offers a rigorous framework for identifying progress and predicting the project completion date based on the quantity of work achieved compared to the quantity planned to be accomplished.

This presentation is part of an ongoing project focused on identifying the challenges, and opportunities created by adapting an improved management approach to control agile, adaptive, and distributed projects focused on optimising resource productivity.

For the last few days, I have been reflecting on winning the Wayne Wilson Award for Lifetime Contribution in Project Controls at the Project Controls Expo Australia held at the MCG, Melbourne (14-15th Nov): https://projectcontrolexpo.com/aus/ and wondering how much of life is crafted and how much is serendipity? See a brief video of the 2023 Awards event.

From a very early age I had decided to follow my Great Grandad, Grandad, Father, and Uncles and become a builder – building things is fun. Then at college in 1970 I became interested in project controls and CPM scheduling (mainframe computers were really cool things to make work). So, after graduating, my career choices were always bent towards project controls on building projects and working for either project controls consultancies, or building companies.

But, ending up in Australia was pure serendipity! In 1972, I had a really good job with a major UK builder and only knew of Australia as the ‘old adversary’ in the Ashes cricket tests. I also used to crew for a friend in his Flying Fifteen (2 person) sailing boat at the Medway Yacht Club and we were doing quite well in the Sunday points series. He had to go away for a weekend and asked me to race the boat to help keep our aggregate points score up. No problem, I just needed to find a crew. One of the people I would normally ask (a 16 stone London Fireman) was at the club, but the wind was very light – I asked John if he knew someone who weighed a bit less and he introduced me to an Australian girl accompanying him and his wife for a day at the club. A slow race on a sunny day (in England….), talking, exchange of contact details, falling in love, and in 1974 I was following Clo to Australia to get married. Some 20+ years later I realized I was supporting Australia in the cricket (and still do).

The other factor that is continuing to shape my development is the help, encouragement, support, and challenges I have received; from family, friends, colleagues, mentors, and honorable adversaries. No one achieves anything alone. The people who have helped me over the decades are far too many to name but a lot of memories have been flooding into my thoughts over the last few days – sadly, in many cases it is too late to express my gratitude. For the rest I need to be more open to expressing the gratitude I feel – thank you!

So, to answer the question posed at the start of this post, luck (or random chance) seems to have a significant impact on everyone’s life (it is better to be born lucky than rich), but everyone also has the opportunity to play the hand fate deals them, their way, to achieve their objectives. No one is perfect, we all make mistakes, cause unnecessary upset, and fail to properly acknowledge people. Correcting the wrongs, and recovering from failures, is as much a key to growth as having clear objectives and working to be successful; but achieving both of these needs help. The good news is everyone can both help, and be helped, by the people around them, you just need to open up enough to let it happen.

My lifetime is not over yet! And, the one thing I seem to be reasonably good at is communicating and writing about project management and project controls in a clear and easily understood way. The world needs good project managers and controls people and with luck I will still be publishing blogs and papers for many years to come. When I started writing and publishing papers and articles there were a range of complex drives, in large part writing is the way I think and learn – but at no time until the last couple of months did I expect this interest to lead to me receiving a ‘lifetime achievement award’. For more on the citation for the award, see more on the PGCS New Page.

The resources at https://mosaicprojects.com.au/PMKI.php is a library of most of my writings to date (and continues to grow), almost all of the papers are free to use under the Creative Commons License which means you can copy, adapt and use the materials in any way that helps you and your career.

In 2018 the Carillion group of companies were bankrupt owing £1.5 Billion ($2.9 billion Australian), at the time, the largest bankruptcy ever in the UK. The latest news is in October 2023, KPMG was fined a record £21 million (AU$40 million) for a ‘textbook failure’ in its audits of Carillion. This long running saga raises questions of ethics both within KPMG and the Carillion Board, and controls. Did the Board and Auditors not know (a management failure), or was it a case of not wanting to know the true situation (a governance failure)?

A wider question for another time is the way the ‘big four’ accounting firms operate. String together Arthur Andersen and Enron in the USA (2001), KPMG and Carillion in the UK (2018), and PWC and the Australian Tax office (2022) suggests there are major structural issues with the ‘big four’ partnership model.

The Carillion Story

Carillion was created in July 1999, following a demerger from Tarmac Ltd., which had been founded in 1903. Following the demerger, Tarmac focused on its core heavy building materials business, while Carillion included the former Tarmac Construction contracting business and the Tarmac Professional Services group of businesses (I worked for Tarmac Construction in 1971/72 – it was a great company in those days).

As an independent company, Carillion undertook a series of acquisitions and expansions including:

2001, expansion into the facilities management services sector

2001, acquired the 51% of GT Rail Maintenance it did not already own

2002, bought Citex Management Services

2005, acquired Planned Maintenance Group

2006, Mowlem support services business

2008, Alfred McAlpine

2008, Vanbots Construction in Canada

2011, Eaga, an energy efficiency business rationalised later in the same year

2012, 49% interest in The Bouchier Group, providing services in the Athabasca oil sands area

2013, the facilities management business of John Laing

2014, 60% stake in Rokstad Power Corporation, Canada

2015, Outland Group, a specialist supplier of camps and catering at remote locations in Canada

2022, Ask Real Estate, a Manchester-based developer

All of these acquisitions came at a cost, in March 2015 concerns about Carillion’s debt situation were raised and by October 2015, Carillion had become hedge funds’ most popular share to ‘sell short’ as analysts questioned the lack of growth and rising debt; the company’s share price fell 19% over the same period.

On 10 July 2017, a Carillion trading update highlighted a £845 million impairment charge in its construction services division, mainly relating to three loss-making UK PFI[1] projects and costs arising from Middle East projects. These and other write downs together exceeding £1 billion occurred only a few months after KPMG had given an unqualified audit opinion on the correctness of Carillion’s accounts.

However, despite these problems, in the five-and-half-year period from January 2012 to June 2017, Carillion had paid out £333 million more in dividends than it had generated in cash from its operations. But, net cash from operations was also needed to pay for investments, and interests on debt (Carillion’s interest charge was £30 million in 2016).

The Carillion Collapse

At the time of its implosion in January 2018, Carillion employed 43,000 people in defence, education, healthcare, transportation and construction and service activities. It had around 420 contracts with the British public sector and many other commercial contracts in the UK and overseas.

Reporting at the time highlighted the aggressive growth strategy, a complex internal management structure, a fuzzy governance structure, poor supervision of daily activities, and the loss of control on some of its flagship projects.

Carillion had liabilities of £7 billion and just £29 million in cash when it went into liquidation. The primary cause of the Carillion collapse is undoubtedly the actions of its directors and managers and there are ongoing court actions against these people. However, the role of an auditor, is to provide an independent assessment of the organisation’s accounts, to identify the types of issue that lead to the collapse of Carillion and provide either assurance, or warnings to both shareholders and creditors.

The KPMG Involvement

KPMG were the auditors for Carillion, their involvement in this saga was finalised a couple of weeks ago when Britain’s accounting regulator, the Financial Reporting Council (FRC), fined KPMG a record £21 million (AU$40 million) for a ‘textbook failure’ in its auditing of the Carillion accounts. The FRC said the number, range, and seriousness of the deficiencies in the audits of Carillion including not challenging Carillion management, and a loss of objectivity were exceptional, which meant that Carillion was not subject to rigorous, comprehensive, and reliable audits in the three years leading up to its demise. The FRC fine would have been £30 million, but was discounted due to admissions and co-operation by the auditor.

In addition to this fine KPMG and its partners have received the following penalties:

KPMG was ordered to pay £5.3 million in costs

The lead auditor for 2014 to 2017 was fined £250,000 and banned for 10 years after a discount to reflect his cooperation and admission of failures.

The lead auditor for 2013 was handed a £70,000 penalty

Three other auditors were respectively; banned for eight years and fined £45,000, banned for seven years and fined £30,000 and banned for eight years and fined £40,000

KPMG was also fined £14.4 million in 2022 after providing false and misleading information to the FRC during spot checks on its audits of Carillion and another UK company

In February, KPMG paid an undisclosed sum to settle a separate £1.3 billion legal claim by the company’s liquidators, who claimed the auditor had missed ‘red flags’ resulting in the group’s accounts being misstated.

The FRC found that KPMG had failed to respond to numerous indicators that Carillion’s core operations were lossmaking and that it was reliant on short term and unsustainable measures to support its cash flows. The Carillion case is the 16th since 2018 in which the FRC or an industry tribunal has imposed sanctions against KPMG. It takes the total penalties and costs levied against the firm in that time to more than £95 million — far more than its rivals.

Conclusions

The lack of press coverage of this saga in Australia at least can be attributed to the coverage of first the referendum, then the war in the Israil, plus the years of investigation and multiple trials since the Carillion collapse in 2018. The still largely unanswered questions include:

Can large organisations really be that bad at controlling major projects? My answer is yes – look at London’s Crossrail project[2], HS2, and a long list of other projects.

A more focused controls question is are the controls failure on this type of project a question of not knowing, or not wanting to know? My answer is in Carillion’s case, the Directors did not want to know! Other situations are likely to vary[3].

Who is responsible for the controls and reporting failures? My answer is the governing body. It is the Board of Directors who set the standards required from management and you do not get good controls without a significant investment[4].

What about the Auditors? My answer is both governments and corporations need to seriously rethink the way they engage with the ‘big four’, and the ‘big four’ need to be completely restructured – the ‘partner model’ has clearly failed.

This webinar presented as part of the free PGCS 2023 Webinar Series looked at two processes that are ‘baked into’ standard project management estimating and control to show how recommended good practices are still optimistically biased.

When preparing an estimate good practice recommends using Monte Carlo to determine an appropriate contingency and the level of risk to accept. However, the typical range distributions used are biased – they ignore the ‘long tail’.

When reporting progress, the estimating bias should be identified and rectified to offer a realistic projection of a project outcome. Standard cost and schedule processes typically fail to adequately deal with this challenge meaning the final time and cost overruns are not predicted until late in the project.

This webinar highlighted at least some of the causes for these problems. Solving the cultural and management issues is for another time. Download the PDF of the slides, or view the webinar at: https://mosaicprojects.com.au/PMKI-PBK-046.php#Process2

The purpose of project controls has been defined as: Project controls are the data gathering, management and analytical processes used to predict, understand and constructively influence the time and cost outcomes of a project or program through the communication of information in formats that assist effective governance and management decision making[1].

The question posed in this short post is how can we fulfil this objective when different processes calculate completely different completion dates for the same set of project data? The options for the calculated project delay for the simple project outlined above are:

– CPM using progress override calculates a 3 week delay.

– CPM using retained logic calculates a 4 week delay.

My suggestion is a realistic prediction of completion needs more than a simple CPM update that assumes all future work will miraculously be completed as planned. WPM (Work Performance Management) has been developed to apply a similar approach to EVM, ES and ED, based on understanding the ratio between work performed and work planned and applying this factor to the future incomplete work to assess the likely completion date if nothing changes.

For the last 13 years I’ve been part of the team developing delivering the Project Governance and Controls Symposium in Canberra. In a couple of weeks’ time from the 22nd to 24th August, we will be celebrating the 10th Anniversary symposium at the Canberra Rex Hotel, for more on this see: https://www.pgcsymposium.org.au/

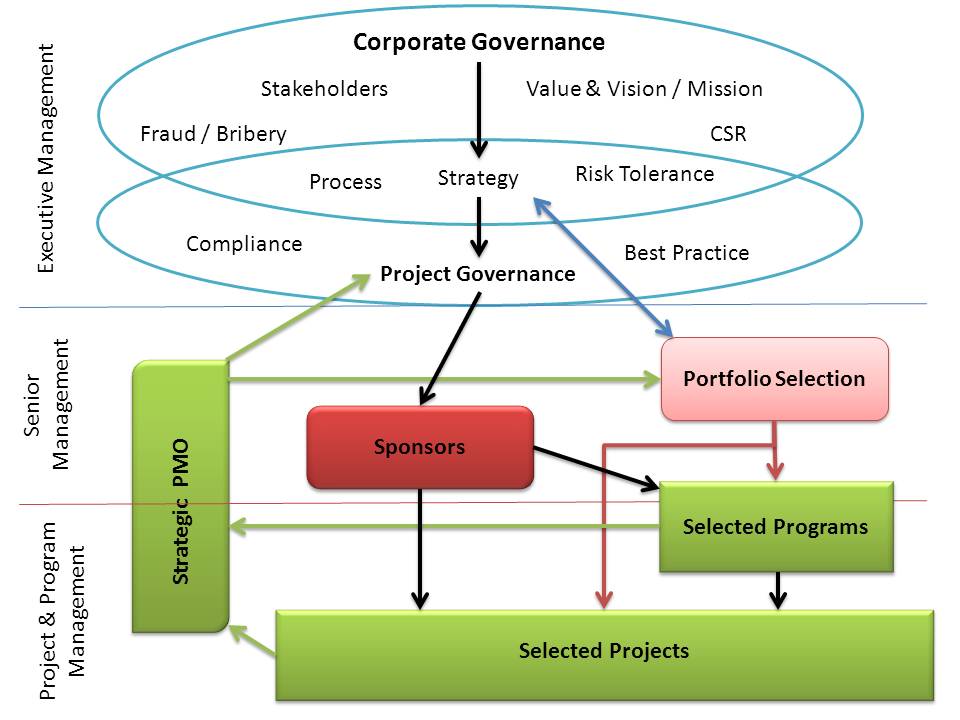

The concept of linking project controls and governance may have been seen as something unusual a decade ago, but as an article in this month’s Australian Institute of Company Directors magazine, the topic is (or should be) of significant interest to both senior managers and directors. In every organization there are a number of projects that are central to the organization’s ability to respond to change, and deliver its strategy. These projects affect the performance of the organization and therefore the performance of the project has legal implications for the organization and its directors and officers. There have been successful prosecutions of numerous organizations that failed to manage project issues effectively.

Director’s responsibilities

Each director has a core responsibility to be involved in the management of the company and to take all reasonable steps to be in a position to guide and monitor management[1]. This requires information, and under the Corporations Act, the director can rely on information provided by the company’s officers and employees, provided the director has reasonable grounds to believe they are reliable and competent people, and the director has made an independent assessment of the information. The legislation also includes a positive due diligence obligation in respect to a number of key business activities including financial reporting, OH&S, and the management of ‘mission-critical risks’.

This means where a project or program has been established to deliver a critical capability the directors need to be across the project and understand its status and predicted outcomes. This of course need information!

Management’s responsibilities

While directors have been subject to legally imposed obligations for decades, management has largely been able to avoid legal liability. This is changing and the legal obligations of company officers and employees who provide information to the board are steadily increasing. The law requires information provided to the board to be complete and accurate.

The Officers of the company will typically include most members of the ‘C-suite’ and may extend to other senior management roles. As an officer, each person is subject to a general statutory duty of care and diligence that applies to all aspects of their role including briefing the board[2].

This was extended in 2019 when the Corporations Act was amended by the Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act to create new civil penalties for both corporate officers and employees who mislead the board by providing incorrect information, or by omitting information. This applies to any employee who ‘makes available or gives information, or authorizes or permits the making available or giving of information’ to a director that relates to company affairs. This provision applies to information in any form, all that is required is for the information to be materially misleading, which includes ‘half-truths’. If the information has been provided without the person taking reasonable steps to ensure that the information is not misleading, they have contravened section 1309 (12) of the Act.

The reasonable steps include the person being able to show they made all reasonable enquiries under the circumstances and having done so believed the information was reliable, accurate, and not misleading. If these duties are breached ASIC can run civil penalty proceedings against the individuals concerned without having to show they knew the information was materially misleading or intended to mislead.

What this means for project controls

Within an organization where the delivery of the benefits, or capabilities, created by projects is a core part of the organizations business strategy, information on changes in the expected delivery date and/or cost to complete important projects is likely to be seen as information that is material to the affairs of the company with a particular focus on its continuous disclosure obligations. Failure to comply with the Corporations Act has consequences for the company[3]. But where the directors were acting reasonably on the information provided to them, liability may well flow down to the officers and employees who provided inaccurate, or incomplete information to the board.

The solution is simple, set up governance and controls systems that provide ACCURATE information[4].

But achieving this is not easy, success requires the right culture, management support, and capable staff. However, even with these factors in place providing correct information is not easy. One of the major challenges is predicting the likely completion date for both ‘Agile’ and ‘distributed’ projects where traditional CPM simply does not work! And without knowing the overall timeframe, any cost predictions are questionable. Using EVM and ES is of course one solution that’s ideal for larger projects; a simpler, more pragmatic option for most normal projects is to use WPM to calculate the current status and projected end date. For more on WPM see: https://mosaicprojects.com.au/PMKI-SCH-041.php#WPM

This is just a brief overview, there are two ways to find out more:

[1] See the ‘Centro case’: ASIC -v- Healey [2011] FCA 717.

[2] In ASIC -v- Lindberg [2012] VSC 322, the former CEO of the Australian Wheat Board admitted to failing to inform the board of key issues.

[3] In 2006 Veterinary pharmaceuticals company Chemeq Ltd paid a $500,000 fine, in part for failing to keep the market informed of cost overruns and delays on a project to construct its manufacturing facility [Re Chemeq [2006] FCA 936].